A Data-Driven Christmas

By Digimid Quant

/ December 20, 2018

‘Twas the week before Christmas at the North Pole

finishing all the project was the Head Quant’s Goal.

Santa was wanting the newest naughty and nice list.

Presents are needed for all good engineers and analysts.

In California, they want a fire restoration tree and plant seeding robot.

In Michigan, they want distribution channels for their new legal pot.

Read More

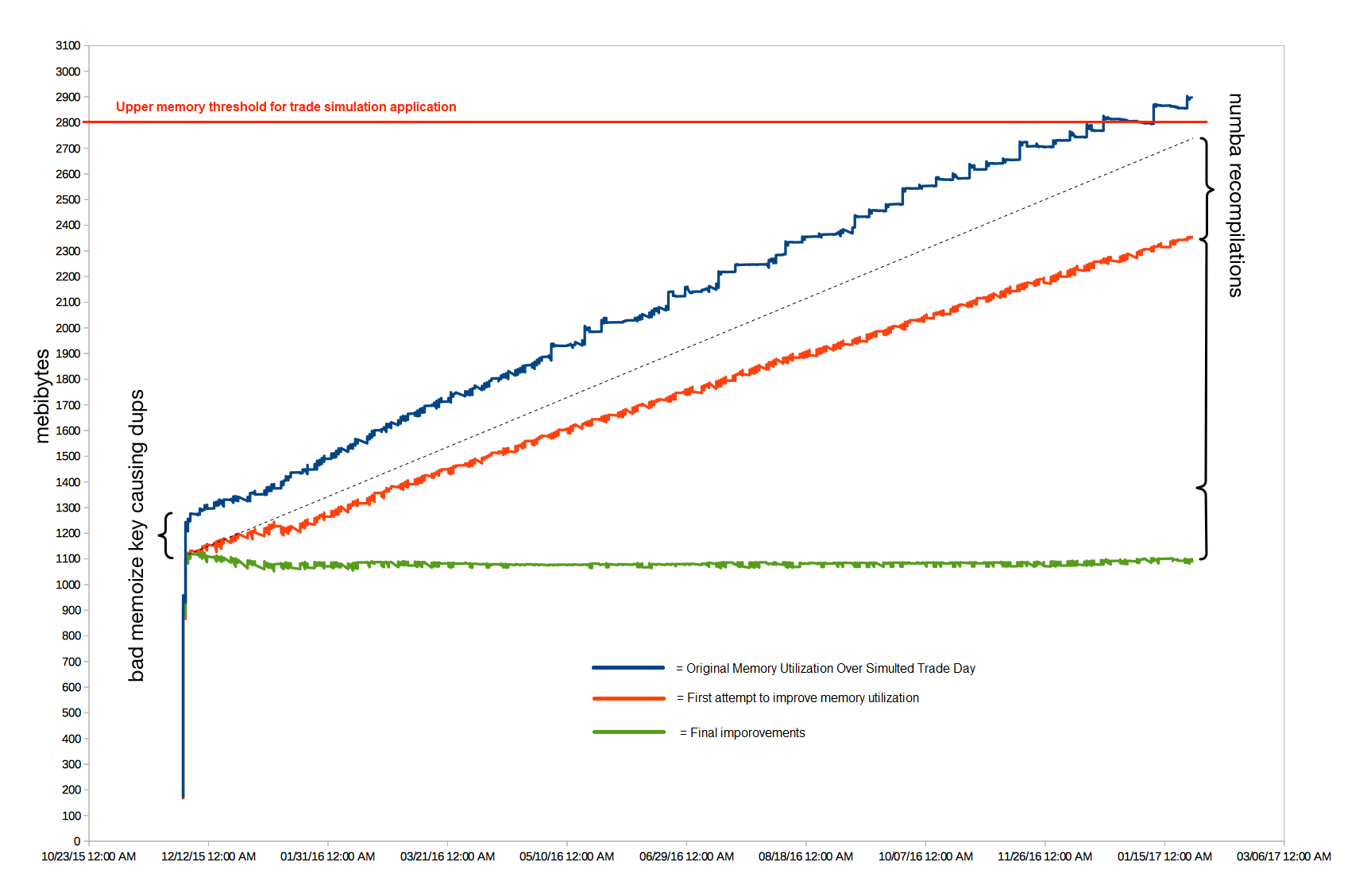

Fixing Python Memory Leaks

By Digimid Quant

/ December 7, 2018

A few of our power users reported that long-running backtests would sometimes run out of memory. These power-users are the people who often find new trading strategies and so we wanted to work with them to improve the performance of our backtesting tools. Over the past couple of weeks, our senior engineer found that the problem wasn't in our code, but in one of the popular Python libraries that we use.

We found the problem in numpy and numba.

Read More

Fintech Capital Markets on CloudQuant’s AI push adds RavenPack for alt-data

By Digimid Quant

/ November 28, 2018

CloudQuant's CEO recently discussed the addition of RavenPack analytics to our trading strategy incubator with Fintech Capital Markets at the Battle of the Quants conference in London.

Topics covered:

* Alpha Signal Studies

* Professional level technology for the crowd to compete with Wall Street

* Bitemporal data access for historical data

* Alternative Data

Read More

Jessica Darmoni's Review of the 34th Futures Industry Association Expo

By Digimid Quant

/ October 19, 2018

The Futures Industry Association (FIA) held their 34th Annual FIA Expo conference at the Hilton Chicago last week bringing together capital markets influencers, regulators and innovators to discuss some of the most pressing matters facing the industry.

Read More

SMB Quant Video 1 – Developing a Model

By Digimid Quant

/ September 19, 2018

Jeff Holden develops algo trading models at SMB Capital in New York. He utilizes CloudQuant extensively during his research and development process. In this video he details his process for developing an idea into a model.

Read More

SMB Quant Video 2 – Democratization of Trading – CloudQuant

By Digimid Quant

/ September 19, 2018

In video two of SMB's new Quant series Paul Tunney discusses why you should use CloudQuant to develop an algorithmic trading model.

Read More

Conversations: Effects of Alternative Data Sets on Trading Algorithms

By Digimid Quant

/ September 6, 2018

What effect can alternative data sets have on trading algorithms? We asked a few of our teammates and systematic traders...

Read More

Roles Played by Bayesian Networks in Machine Learning

By Digimid Quant

/ September 5, 2018

Bayesian Network is a probabilistic graphical model which comprises variables and its relationships. It uses Bayesian inference and learning to develop the algorithm.

Read More

AI & Machine Learning News. 03, September 2018

By Digimid Quant

/ September 4, 2018

Baidu launches a simple AI training platform, simplification is the future, our new offering Cloudquant.AI will make it easier than ever for Data Scientists and Traders to identify/create profitable indicators and utilize or share them for profit. Detecting DeepFake to Thanos to Everyone Can Dance, how AI and ML are making it difficult to believe your eyes. Predicting Popularity of The New York Times Comments with effective use of a python sentiment library. Hardware Stocks to Outperform the Market, can you do better on CloudQuant? Finally, how to approach speech recognition in languages with fewer native speakers, Facebooks method vs an individual Data Scientist.

Read More

Conversations: Recommendations to Someone Starting out at CloudQuant

By Digimid Quant

/ August 13, 2018

The CloudQuant team discusses their helpful thoughts for beginners on CloudQuant. We want to boost everyone starting out on our platform in their algo development and backtesting.

Everyone in our company uses the CloudQuant website and coding platform in one way or another. We all use our own application, just like the crowd researchers. When we say that our free backtesting tools are "institutional grade" we really mean it. Every algo we run in our trading and investment strategies is proven in the same backtesting engine as the crowd uses. We rely on the scorecards, the reports, and the simulated trades to ensure that our trading is successful.

Read More

Conversations: Learning Python within CloudQuant

By Digimid Quant

/ August 7, 2018

What was your experience like learning Python within CloudQuant?

We asked our portfolio managers and product management teammates who code in Python to explain their starting experiences in programming with Python with CloudQuant. We wanted to share with everyone what encouraged them to keep learning throughout the years.

Everyone here codes as part of their job. This includes the CEO all the way down to the interns. We rely on our Backtesting Engine to ensure that trading algorithms work well before committing money to the automated trading strategies. But we also use JupyterLab in our daily work. We generate our reports, monitor our systems, and do all sorts of tasks in Python. Python has overtaken the spreadsheet in CloudQuant.

Read More

Conversations: What we wish we knew when we started AlgoTrading

By Digimid Quant

/ July 30, 2018

CloudQuant's portfolio managers and quantitative algo traders look back on their starts in Algorithmic Trading. This candid overview allows everyone to see the "Things We Wish We Knew When We Started AlgoTrading". This is a short collection of the interviews with some of our amazing coders here in the office

Read More

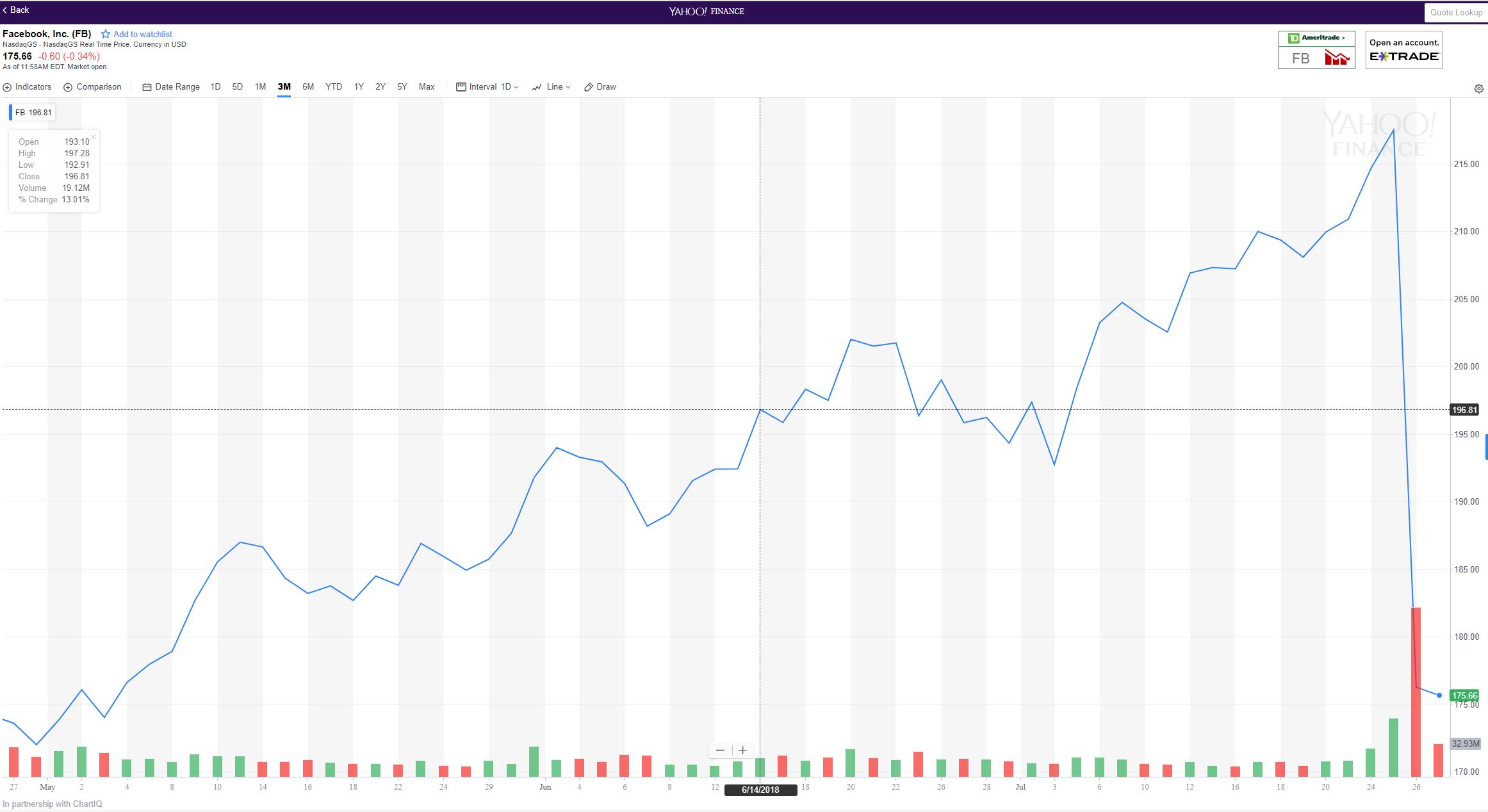

$FB Decline 19%- What did the Social and technical analysis show? – July 26 2018

By Digimid Quant

/ July 27, 2018

$FB's 19% drop was preceded by TA-LIB and Social Market Analytics indicators to sell. The $120 Billion drop in market cap could have been an opportunity to short sell before the market close the previous night.

Read More

Google Wants to Dominate AI in 2018. Here’s Why

By Digimid Quant

/ July 23, 2018

Google Wants to Dominate AI in 2018. Here's Why Let’s get this out of the way: ever since the 2001...

Read More

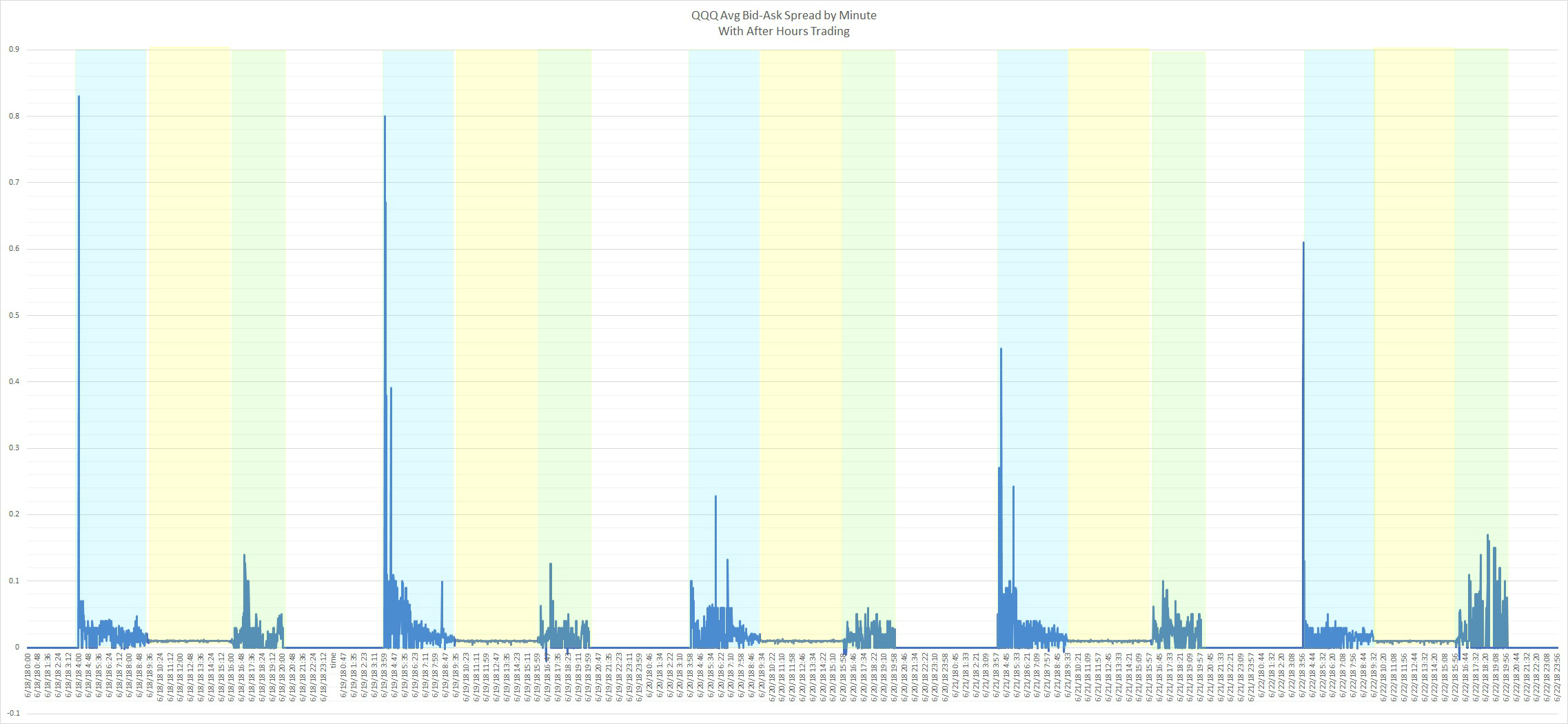

US Stock Market pre-market and post-market bid-ask spreads are different than regular trading hours

By Digimid Quant

/ July 13, 2018

Regular Trading Hours in the US Stock Market is 9:30 a.m. - 4:00 p.m. Trading can happen in the pre-market hours (4:00 a.m. - 9:30 a.m. ET) and in the After Hours market (4:00 p.m. - 8:00 p.m.). The free historical market data in CloudQuant allows you to examine the spread data and the differences between sessions.

Read More